The SBA has begun the process of reaching out to individuals who may be eligible for the Covid-19 Targeted EIDL Advance, inviting them to apply for the additional funds.

If you received an invitation to complete the application, this post is here to help you walk step by step through how to fill out the application for the Covid-19 EIDL Targeted advance grant, focusing especially on independent contractors with gig economy apps like Doordash, Instacart, Uber Eats, Grubhub, Uber and Lyft and others.

Note that this is written with a particular focus towards independent contractors and self employed individuals. I write especially about the business side of being a gig economy contractor.

If you run or manage a larger business, hopefully this can still be helpful for you. Just be warned that some of this content focuses on contractors who do not have employees, so some things may be different for you.

Warning: This is a LONG article. I include a lot of text from the SBA email and application. Use your own judgment to determine how much to read through, and how much to skip past.

I will post the outline here to let you jump ahead if you prefer. Here’s what we’ll cover:

- What is this grant, and are you eligible?

- Things to do before you apply

- How to fill out the targeted EIDL advance application step by step:

- What happens after you are done?

What is this grant, and are you eligible?

The targeted EIDL advance was something added in the stimulus package passed late December of 2020. As of mid February, the SBA is just now getting around to processing applications.

The purpose of this targeted advance is to provide a larger amount of relief to businesses, sole proprietors and independent contractors who received less than the full $10,000 advance that was part of the original Covid-19 EIDL advance from early and mid 2020, and who were truly impacted by the pandemic.

Priority in this round of funding will be given first to those who received the earlier advance but did not receive the full $10,000. Second priority will be those who applied but never received an advance due to lack of funding.

The difference between the targeted grant and the advance given out earlier in 2020

In some ways you could say the targeted advances are an effort to ‘make whole’ the previous advances under the CARES Act earlier in 2020.

The intent of the act was to have all businesses receive a $10,000 advance that did not have to be paid back. The SBA later added the rules that defined that it would be $1,000 per employee up to ten employees.

Independent contractors and self employed individuals were eligible for the grant. However, those of us who don’t have employees could only receive a $1,000 advance. And that’s all we received, if we did apply.

The purpose of the targeted grant this time around is to complete that original intent for businesses who truly were impacted by the pandemic. Thus, if your business received less than the $10,000 the first time around AND you can demonstrate the need as defined by the new criteria, you may qualify for an additional advance or grant.

The total of the original advance and the new grant are not to exceed $10,000. Language in the latest act specifically states that funds are not to be based on the number of employees.

As I write this the only thing that is not completely clear is whether there are other limits on the funding. In particular, some loans that were approved (based on 2019 income) beyond the advance were less than $10,000. I haven’t seen language that addresses whether the grant would be limited to whatever the approved loan amount would be.

What are the new criteria?

The latest act added three new criteria.

- Your business has to be in a low income community.

- You have to demonstrate you had an economic loss over an 8 week period compared to the same 8 weeks of the year before.

- You have to have less than 300 employees.

For those of us who are independent contractors with Doordash, Uber, Instacart, Lyft etc., the 300 employee thing is obviously not an issue. The original limit was 500 employees. If your business is part of this first round, has received an advance before and you do have a lot of employees, chances are you already received the maximum.

Your business address needs to be in a low income tract. For most of us who are 1099 contractors, that’s your home address. You can get more details about what it means to be in a low income area and how to find the specific details for your area here.

The economic loss piece gets a bit trickier. In the original application, you only needed to have information off your 1099 from 2019. This time around you need much more specific week by week numbers.

The criteria is that for any 8 week period after March 1, 2020, if gross earnings were more than a 30% loss compared to the same 8 week period of the year before, you would qualify. That’s the earnings before expenses are taken out. You can read more about economic loss reqirements here, or you can access the tool we put together where you can enter your weekly income and identify if there’s an 8 week period where you had a loss.

Where do you apply?

You don’t.

You have to get an invitation.

This is a “don’t call us, we’ll call you” kind of thing. There is nowhere to go after this particular grant, you have to be invited by the SBA in order to apply for the targeted advance.

Remember that the priority for the additional funds is to go first to those who received the initial advance, then second to those who applied but then grant funds were no longer available. The SBA has your information, and they will reach out.

The invitation email.

They have started sending out the email to invite people to verify information and to provide a first round of information.

Read the email carefully. I’ll include a lot of it in this article. However, in the event it does change, if you do get the email, read through it. There’s a lot of information that is important to know.

I’ll post some screenshots. It’s a really long email otherwise.

Introduction.

Depending on the screen you’re looking at, it might be hard to read this. So here’s the quote:

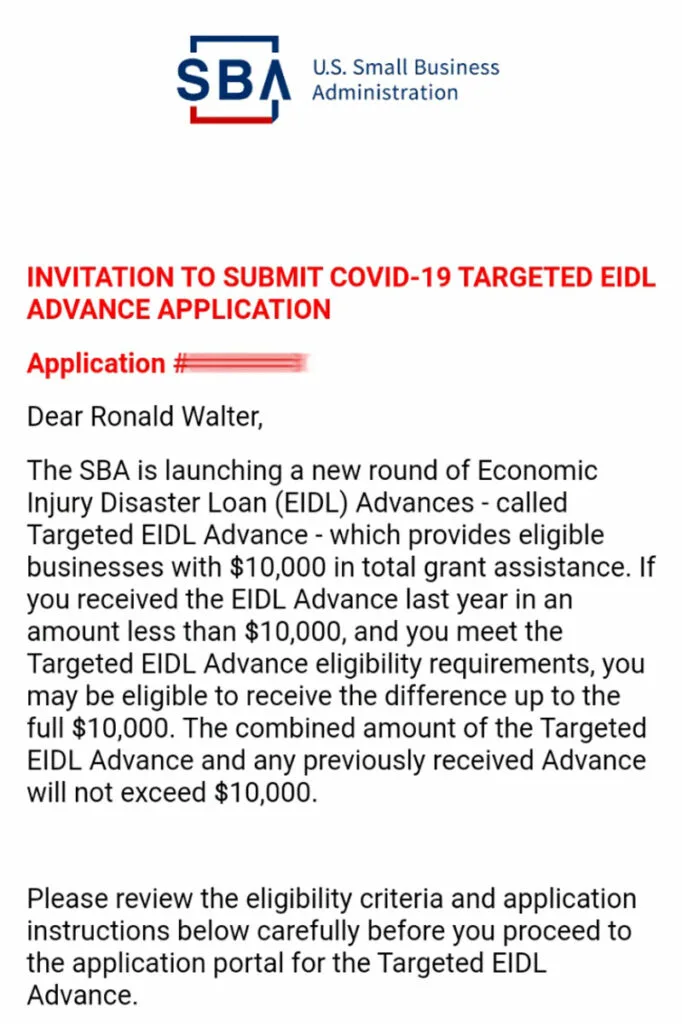

INVITATION TO SUBMIT COVID-19 TARGETED EIDL ADVANCE APPLICATION

Dear ______

The SBA is launching a new round of economic injury disaster loan (EIDL) Advances – called Targeted EIDL Advance – which provides eligible businesses with $10,000 in total grant assistance. If you received the EIDL Advance last year in an amount less than $10,000 and you meet the Targeted EIDL Advance eligibility requirements, you may be eligible to receive the difference up to the full $10,000. The combined amount of the Targeted EIDL Advance and any previously received Advance will not exceed $10,000.

Please review the eligibility criteria and application instructions below carefully before you proceed to the application portal for the Targeted EIDL Advance.

Additional sections of the letter.

The email went on to lay out criteria for the grant. A screenshot of that criteria is shown in the eligibility portion of this post above.

We recommend that you have a copy of your 2019 Federal Tax Return on hand to assist you in completing the Targeted EIDL Advance application questions. You will also be asked to confirm that the information provided in your original EIDL application is still accurate. If there are any changes, you may be asked to provide documentation in order to determine if you are eligible for a Targeted EIDL Advance. Applicants that pass the initial eligibility requirements will also be required to electronically sign an IRS Form 4506-T allowing SBA to obtain tax transcripts directly from the IRS before we can approve your request for the Targeted EIDL Advance.

SBA’s goal is to process all requests within 21 days of receiving a completed application. All application decisions will be communicated via email. Due to limited available funds for the Targeted EIDL Advance program, SBA will not be able to reconsider applications through an appeal process, so please make sure that your information is correct when submitting your application.

I’ve heard comments that the original grant was funded almost immediately, and this time they’re saying 21 days out. I think this is reasonable considering they have to verify eligibility. That can be time consuming.

The rest of the email gets into some important things you need to know about having the right banking information. I’ll add some more screenshots of that information below.

What if you never received an email?

Wait.

This is taking some time to roll out. I first started hearing of people getting their invitation about a week ago. I think they’re doing this in waves to make sure they get it working correctly.

If you received the initial grant and haven’t received an invitation email, double check that the email you used for the initial application is good. Check your spam filters or promotional folders or anything like that.

The thing to watch for is when the SBA begins moving on to second priority applicants. That would indicate they’ve moved through everyone who originally received the grant. I’ll try to stay on top of events and will update this section if I hear that has happened.

If you feel you should have received an invitation and do not get one by March or so, you may want to contact the SBA. You can contact them at TargetedAdvance@sba.gov or by phone at 800-659-2955. As I mentioned at the start of this section, the first thing is wait. It’s going to take some time. If you reach out now (mid February) you may not get a response yet.

What if you never received a grant the first time?

If you applied before December 27, 2020 but did not receive the advance due to funds being out, you are next in line. The same answer holds for you: wait.

The SBA is first moving through everyone that did receive the advance. Once they’ve covered all of those, they’ll move on to you.

If you did not apply for the EIDL program at all, it does not appear there will be anything in this round that you qualify for. They do not seem to be opening up new applications.

Things to do before you apply

If there’s one thing we learned from the original release of the EIDL and PPP programs, it’s to act quicly.

If you receive the invitation email, do not waste time responding. They make a point to say that funds are limited.

My recommendation is to make sure you have your information ready ahead of time. In particular you want to make sure you have your financial information together and make sure you have all the information for your bank account (and the right kind of bank account).

The thing is, you want to get it right. A lot of people who applied for funding under the Paycheck Protection Program and the EIDL did not receive funding for one reason: They were sloppy with their application. They put the wrong information down about their business or about their bank account.

I read more people comment in forums about problems with their bank info when they applied the first time around. By the time they had everything straightened out, funds were gone.

Get your stuff together. Get it right. Treat this like a business application, not some quick easy survey you’re getting money for. Do it right and you greatly increase your chances.

1. Know what you made monthly.

Interestingly, the burb from the email above states that you want to have your 2019 tax return handy. When I ran through the application, there wasn’t anything that required info from my tax return.

However, they did ask for my monthly income from 2019 on.

To be fair, the part of the email that tells about qualifications says you will need this. It says you must have:

Suffered economic loss greater than 30 percent as demonstrated by an 8-week period beginning on March 2, 2020, or later, compared to the previous year. You will be required to provide the total amount of monthly gross receipts from January 2019 to the current month-to-date.

SBA’s invitation to apply email, section on criteria for the targeted EIDL advance.

I’m curious. Will they follow up with a request for weekly totals? Or are they going to stick with the broadest (and simplest) possible scope where they look at 8 weeks as two months.

What if your period of economic loss begins in the middle of a month? Will that disqualify some who should otherwise be qualified?

Understand what they mean by gross receipts.

The terminology really throws people off.

“Gross receipts” does not refer to those restaurant receipts that are covered in grease and food stains. While those are indeed gross, that’s not it.

In accounting terms, that’s your money received after cost of goods sold.

Put real simply, for those of us who are gig economy contractors, that’s the money you received from Doordash, Uber Eats, Instacart, Uber, Lyft, Grubhub or other gig apps.

If you do other work, such as flipping merchandise on eBay or Amazon, gross receipts is what you received for your sales minus the cost of buying the items.

This is not the same thing as your net profit. Gross receipts is your money BEFORE your expenses.

Note: If you had more than one schedule C, you’ll need to add up the gross revenue from all of them.

Get your finances organized.

You’re going to have to go back now and look up your earnings, month by month, since January 2019.

If you haven’t been doing this so far, this is a good time to put it into a program that will give you a proper report. Chances are the SBA is going to ask for documentation of these monthly amounts.

For independent contractors, you’re probably going to need one or both of the following:

A monthly profit and loss report. If you are using a program like Quickbooks, you can pull up a report and choose to show monthly columns. It would look something like this:

You can get this kind of report on Quickbooks Online or the Desktop version. Other programs like Freshbooks or Wave also have this ability. Even GoDaddy Bookkeeping will give you a monthly breakdown.

Some programs like Hurdlr and Quickbooks Self Employed will require you to run individual Profit and Loss statements for each month.

And then there’s Stride. Forget about it. There’s no reporting capability. All you can do is download the data and do the math.

If you had more than one schedule C, you’ll want to run your numbers for all of your businesses individually.

Bank records.

In some of their guidance, the SBA has talked about bank records as one form of documentation.

I don’t know yet if the P&L statements will suffice. For that reason, I recommend you go ahead and get your bank records together now. Here’s what I would recommend:

- Download your bank statements for each month. If you had more than one bank where payments were made, download those as well.

- Highlight every payment that came in for the month.

- Make a list of the dates and the amounts of payments received for each month and attach that to your statement.

- Add up the totals and make sure they line up with your income reported on your 1099. Because if they don’t match up, you may have to provide an explanation.

2. Make sure you have the right kind of bank and correct bank information.

The SBA makes a big deal of this in their email. They point out that one reason a lot of applications don’t get approved is because it’s impossible to transfer funds based on the information provided.

Whether this is a legitimate excuse or not, here’s the thing you have to understand: The SBA is overwhelmed trying to get all this processed. They’re having problems with the PPP program. They’re delayed on EIDL.

They don’t have the manpower to hunt down bad bank account information. Whether they should or not, that’s another discussion.

Have your act together now so they can’t make that excuse.

The SBA Email:

Here’s a screenshot of that section:

I told you they make a big deal out of it.

This is seriously nearly half of the entire email, and it’s all about just making sure you have the right information.

I won’t quote the entire thing but here’s what it boils down to:

It is very important that you double-check your bank account information carefully before submitting. Incorrect or incomplete information may result in an inability to approve your request or successfully disburse your funds. Carefully review the information below regarding bank account deposits.

SBA invitation email for targeted EIDL advance application, section on having correct bank information.

Take this seriously. If you screw this up there may not be an option to go back and get it right later.

Here’s a summary of the points they make in the email:

- Double check that your account and routing number are correct. (Comment: this is a no brainer, but you’d be surprised how often it’s an issue)

- Make sure that the account can have ACH payments.

- Get the bank name correct. Find out the official name of the bank.

- Make sure this is for a CHECKING account.

- Ensure the account is open and can take payments.

- Make sure account holder details match up with the information provided in the application.

I have to be honest. I read through this and I think… do they really have to stipulate all this? When you read the language they used, you can tell that these were common problems during the first round of applications.

In a nutshell, here’s what it boils down to:

Use an account that is yours and that the details match your contact information and name provided on the application.

Get the account details right.

Make sure it’s a checking account that can accept ACH payments.

And oh, by the way… Get the account details right.

How to fill out the targeted EIDL advance application step by step:

It really was pretty simple to walk through the application. Since this is all sent out to people who have already been through the EIDL process, most of it is done for you. I’ll walk through what was all on the application.

I won’t bother with the link, because every link is personalized. It looks like this on the email.

Hit the button. Enter your social security number (or EIN if you used one on your first application). And away you go.

Eligibility questions

We start off with 23 questions. Most of these are pretty simple and straight forward. You can’t be involved in certain kinds of business. You can’t be a criminal.

And then there are a few other things that might surprise you.

Here’s a screenshot of the whole set of questions. Then I’ll comment on questions to clarify where it seems necessary. Some questions probably need no explanation.

Introduction to the eligibility questions

Applicant must review and respond to all of the following questions. Please note that “owner” includes each proprietor, each limited partner or LLC member who owns 20% or more interest, each general partner or managing member, and each stockholder or entity owning 20% or more voting stock. If applicant does not meet the initial eligibility requirements, Applicant will not be able to proceed to the remainder of the application.

Introduction to Eligibility Questions on the Targeted EIDL Advance application.

Note from this that generally you are answering for yourself. If you have a legal partnership or an LLC with more than one member, you need to answer related to all owners.

One other thing that may lead to some confusion. Applicant refers to the business, not to you as an individual. That’s an important distinction in some future questions. If you read “Is the Applicant,” read it as “Is the business.”

What about if you have more than one business?

Every year, I submit two Schedule C forms with my taxes. One is for my delivery work. The other is for my website and online marketing. That’s because all of the miles I drive are not consistent with online work, but all the website costs and office costs are not consistent with delivery work.

What do you do if you have more than one business on some of these questions? Which business are we talking about?

If it’s a business that you’re filing information on as part of your individual tax return, the best answer is “all of them.”

In their guidance on documentation for Revenue Reduction in the Paycheck Protection Program, the SBA kind of backs up this idea. In a footnote on Page 4 they mention that if you have multiple schedule C’s, you need to add revenue from all of them.

If you file multiple Schedule C forms on the same Form 1040, you must include and sum across all of them.

Footnote 5, page 4 of SBA Guidance on How to Calculate Revenue Reduction on PPP Loans.

I’m looking for similar documentation on the EIDL but since they are both administered by the SBA, I’m pretty sure they’re the same.

If you’re required to add up all revenue on all your Schedule C’s, it’s safe to say that you should be answering the questions based on all businesses, not just one. I think that will be most relevant in questions 11 and 20.

1. Are all owners of the Applicant US Citizens, non-citizen nationals, or qualified aliens?

That first phrase backs up what I was saying. “Are all owners of the Applicant.” Read it as “Are all owners of the business.”

If you are filing as a self employed individual or sole proprietor, answer only for yourself. If you have a legal partnership where an ownership structure is defined, then you’ll need to answer for all your owners.

The bottom line is, are you able to work in the US legally?

2. Is any principal of the Applicant with a 50 percent or greater ownership interest more than sixty (60) days delinquent on child support obligations?

3. In the past year, has any owner of Applicant been convicted of a felony committed during and in connection with a riot or civil disorder or other declared disaster?

If you stormed the Capital and got busted, you need not apply. If you committed a felony during any of the unrest or related to a disaster, you can probably stop right here.

4. Has the applicant or owners of Applicant ever been engaged in the production or distribution of any product or service that has been determined to be obscene by a court of competent jurisdiction?

While this seems straight forward, make sure that the key here is “determined to be obscene by a court of competent jurisdiction.”

5. Is Applicant or owners of Applicant currently suspended or debarred from contracting with the Federal government or receiving Federal grants or loans?

6. Is any owner of the Applicant currently incarcerated?

7. Is any owner of the Applicant presently subject to an indictment, criminal information, arraignment, or other means by which formal criminal charges are brought in any jurisdiction for any felony?

I’m not a lawyer, but I would take this to mean, have you been arrested and being charged for a felony?

8. Within the last 5 years, for any felony involving fraud, bribery, embezzlement, or a false statement in a loan application or an application for federal financial assistance, or within the last year, for any other felony, has any owner of the Applicant 1) been convicted; 2) pleaded guilty; 3) pleaded nolo contendre; or 4) commenced any form of parole or probation (including probation before judgment)?

Have you been convicted of a felony or did you plead no contest to a felony? This isn’t about whether you were ever charged, just if you were convicted or placed on probation for a felony.

9. Is Applicant engaged in any illegal activity (as defined by Federal guidelines), including selling recreational or medical marijuana?

Understand the distinction here that they’re asking about the Applicant. That means your business, not you as an individual.

You’re thinking “wait, marijuana is legal where I am.” I’m sure someone somewhere reading this might work at a dispensary. Why do they say illegal?

Even though states have legalized it, the Federal government hasn’t yet. Businesses engaged in the sale of marijuana are not eligible. This is an important distinction.

The question at hand is, is your business, for which you’re applying, involved in the sale of marijuana? This article is geared mainly towards gig contractors – and unless your gig actually deliveres marijuana, you’re probably okay here.

10. Does Applicant present live performances of a prurient sexual nature or derive directly or indirectly more than de minimis gross revenue through the sale of products or services, or the presentation of any depictions or displays, of a prurient sexual nature?

If you’re operating a strip club or porn or selling stuff around all that as part of your business, you may not qualify.

11. Does Applicant derive more than one-third of gross annual revenue from legal gambling activities?

Maybe you won big in a poker tournament. Does that mean you can’t apply because of this? After all, didn’t we say “Applicant” means your business?

Check out the section before the first question. The SBA requires you to add information up from all of your Schedule C forms. If you reported profit and loss on a Schedule C for gambling winnings, my understanding is you have to include your gambling financials as part of your bsuiness.

12. Is Applicant primarily engaged in political or lobbying activities?

Here’s another one where it’s important to recognize “Applicant” as the business. You as an individual are not prohibited from political activity. It just means a lobbying business can not receive this assitance.

13. Is Applicant owned by a state, local, or municipal government entity (other than a tribal business concern, as described in 15 U.S.C. 657a(b)(2)(C))?

14. Is Applicant owned by a member of Congress?

I wonder, are there any members of Congress who are doing Doordash or Uber Eats as a side hustle?

15. Is Applicant an agricultural enterprise (e.g., farm), other than an aquaculture enterprise, agricultural cooperative, or nursery?

16. Is Applicant a nursery farm that derives 50% or more of annual receipts from the production and sale of ornamental plants and other nursery products that they grow?

17. Is Applicant a pawn shop that derived more than 50% of the prvious year’s income from interest?

18. Is Applicant engaged in lending or investment?

I have to admit, the first time I read this question, I was thinking, “wait, what?”

I’m not sure my meager Roth IRA contributions could be called investing. But still, are you saying I can’t invest?

Remember, Applicant means your Business. Is investing the nature of your business? Now if you’re trying your hand as a day trader and reporting the profits and losses on a Schedule C, you might be. But as a delivery or rideshare contractor who has some investments as an individual, that’s different than investing being a part of your business.

19. Is Applicant a loan packager that earns more than one-third of its gross annual revenue from packaging SBA Loans?

20. Is Applicant engaged in multi-level-sales distribution?

Are you involved in multi level marketing? Think Amway, Herbal Life, Mary Kay, Avon, Primerica. The SBA doesn’t allow financing if involved in network marketing.

But how do you define this?. The FTC has a document that has some guidance involving pyramid schemes and what qualifies. Even that isn’t real clear.

Does it matter though if your business is actually gig delivery or rideshare? Based on information I mentioned above about how the SBA wants you to handle multiple Schedule C’s, if you filed a Schedule C for your network marketing business, it appears you do have to answer based on that.

If you are engaged in a network marketing company and you wonder if you are impacted by this question, you may want to reach out to resources there and find out what they would advise.

Since this blog is about third party delivery, I’ll bring this one up. I’ve talked a little about TripDelivers, a company that recently launched deliveries in Nashville with supposed plans to go nationwide.

I’ve seen some accusations that they’re really a multi level marketing company. I notice they’re listed in a report on a website called MLM Gateway. There are some things about their pay model that bear some resemblance to MLM plans. The question is, does the SBA consider them a MLM company? I doubt they do, but how do you know?

21. Is Applicant engaged in real estate development or investment (other than rental properties)?

Again, this question is about your business. Because you personally invested in an REIT does not mean that your business is engaged in this. The determining factor is, are any of the income and expenses on your Schedule C related to this type of business.

22. Is Applicant a life insurance company?

24. How many employees does Applicant have as of the date of this Targeted EIDL Advance application?

I wrote about this related to the original EIDL application process. At the time I wrote that as self employed individuals or sole proprietors, we have no employees. I also linked to this article from Gusto that said “If you’re a sole proprietor and don’t have any employees, put zero.”

If you said 1 the first time you applied, and you received the advance, it’s obvious that listing 1 was not a problem. If you remember for sure what you put down the first time around, I don’t imagine it would be bad to stay consistent with what you put on your original application.

However, if you’re not sure, zero isn’t a bad answer to go with.

Verifying information from your original application

Once you’ve checked through your eligibility, you move on to this screen.

It’s pretty straight forward. All of this is information from your previous application. If you were funded, there’s less likely to be any issues. However, pay attention to their instructions.

Once again, the print is small. I won’t walk through all the fields because it’s information you previously provided. I am going to break up the introduction paragraph into bite sized chunks because it’s important stuff.

Confirm information is still accurate.

The information below was submitted with your previous application. Please confirm that it is still accurate for your business or organization. Revise any information that has changed.

For most of us things probably haven’t changed much since applying. However, if you’ve had an address change or other contact information has changed, be sure to update that here.

If you do have a different address, make sure you match up with what you will put on your income tax return. The only time you would have a different address that I can think of than your personal address is if you actually rent out an office to operate your business out of.

Do not make up an address just to try to qualify for the low income area qualification. A change of address from a non qualifying address to one that does qualify could easily raise a red flag. If you did make a move, prepare to have documentation that proves your new address.

Get the right business name.

Ensure that the legal name of your business is entered correctly and that it matches your 2019 tax return; this would be the business owner’s name in some cases, such as a Sole Proprietorship or Independent Contractor, where a separate business tax return is not filled.

Just the fact that they have to spell this out tells me this tripped a lot of people up on the original application.

I feel the need to show this. This was from the original application:

I kind of ranted on this when I posted a guide for applying. I did all the “online shouting” posting in Red and using all caps.

Do not, I repeat, DO NOT put Grubhub or Doordash or any other company down for the business name.

My commentary, in all its italicized capitalized boldened glory, on what to put down for Business Name on the EIDL Application.

So I find it interesting and a bit humorous that they felt the need to go into detail on this this time around. That makes me think a lot of people put the wrong thing down here under business name.

I wonder how many didn’t get approved.

Get the right bank information down.

Does this sound like beating a dead horse? Given the amount of space the SBA dedicated to this topic in their invitation email, they’re consistent by addressing it again.

Bank name should be the official name of the bank; please contact your bank if you are unsure. Ensure that you provided a checking account to facilitate the ACH payment.

The bank account you provide must satisfy the following: (1) Account opened using your business legal name; (2) Account has your business address and phone number; (3) Account opened using your business tax identification number (EIN, or SSN if no EIN registered).

One line here is interesting to me:

“Account opened using your business legal name;”

Go back to the line before. If you’re filing under your social security number, as most of us in the gig economy are doing, your business legal name is YOUR name.

So guess what happens if you put “Doordash” down as the business name and the SBA sees your bank account isn’t under Doordash?

Pay attention to what you’re filling in here. Make sure you’re putting the right kind of bank information in, which won’t be an issue if you did your prep correctly.

Entering your monthly income totals

Once you’ve confirmed information from the previous information, you’ll come to a section they call “NEW INFORMATION.”

Complete the monthly gross receipts for each year listed on the form. Gross receipts include all revenue in whatever form received or accrued, from whatever source. If there was a period with no sales, please enter 0.

It’s interesting. The act states that economic loss is for any earnings after March 2, 2020, however they ask you for earnings back to January on this form.

I’m also a bit intrigued that they didn’t ask for weekly earnings.

Note that there’s a space for January, 2021. You’ll need to fill that in as well. If you fill this out in March, it’s possible you’ll need to enter information for February, and so on.

Remember that if you have multiple schedule C’s, you’ll need to make sure you have added up your gross reenue for all of them.

We got into more detail on what gross revenue was up above.

Signing off

Once you’ve done this, you get to the final screen.

Pay attention to what you’re agreeing to here. You’re stating you realize that you’re submitting this under penalty of perjury.

Warning: Any false statement or misrepresentation to SBA may result in criminal, civil or administrative sanctions including, but not limited to: 1) fines and imprisonment, or both, under 15 U.S.C. 645, 18 U.S.C. 1001, 18 U.S.C. 1014, 18 U.S.C. 1040, 18 U.S.C. 3571, and any other applicable laws; 2) treble damages and civil penalties under the False Claims Act, 31 U.S.C. 3729; 3) double damages and civil penalties under the Program Fraud Civil Remedies Act, 31 U.S.C. 3802; and 4) suspension and/or disbarment from all Federal procurement and non-procurement transactions. Statutory fines may increase if amended by the Federal Civil Penalties Inflation Adjustment Act Improvements Act of 2015.

I hereby certify UNDER PENALTY OF PERJURY UNDER THE LAWS OF THE UNITED STATES that the above is true and correct.

In other words, they’re not playing games here.

Do not be sloppy about this. Don’t guess. Don’t go off the cuff. Have your numbers together. This is a business application with a government agency. Treat it that way.

And don’t be tempted to fudge the numbers to make it so you qualify. That’s when you’re really getting in trouble.

What happens after you are done?

Now you wait.

The invitation email said it could be up to 21 days after you submit your application.

If your application meets threshold eligibility requirements for the Targeted EIDL Advance, you will receive an email requesting that you log in to the customer account portal to complete and sign a Request for Transcript of Tax Return (IRS Form 4506-T) for your business or organization. You must complete this task in order for your application to be considered. Submitting this form does not guarantee that your application will be approved.

Here’s what it looks like will happen:

They will check your business address and see if it meets the Low Income Area criteria.

Then they’ll check your income that you submitted. I don’t know if they’ll drill down further into week by week numbers. If you have two consecutive months in 2020 (or 2021) that added up to more than a 30% loss of revenue when compared to same two months the year before, then it’s safe to say you met the 8 week criteria.

If it’s close, will they ask for more detailed weekly information? I don’t know.

The language in their closing paragraph indicates tehre will be a follow up if you appear to qualify. Part of that will be to let them pull up your tax records.

The thing is, tax records don’t give any month to month information. The only thing they can do with that is compare them to your total earnings.

So it’s a good idea to make your monthly totals equal what you put on your tax forms.

When I find out if they are asking for other supporting documenation, I’ll update this information accordingly.

Other than that, now it’s just wait.

Thi

Tuesday 13th of April 2021

After reading all of your comments, I realized I made a huge mistake on my application. I had 2 job but my main job is independent contractor. My W2 job was only part-time. However when calculating my monthly payment, I added 2 jobs together. I should only counted my Schedule C income. What should I do now to correct it? Please advise.

Marc

Friday 26th of March 2021

Thanks for this detailed explanation. I came here to figure out if the $1,000 I made over the summer doing p/t work with the 2020 Census needed to be included in my earnings. I couldn't find any "guidance" (new word for the decade). You touched on it here and the explanation makes sense - this money has nothing to do with my rideshare and gig earnings.

The $1,000 was just enough to bring my overall income JUST BELOW the 30% loss requirement. I recreated the monthly table that the SBA has in their Targeted application process. My heart sank. That's what caused me to look for an answer. By not including the $1,000, one of the "8 week" periods came in at -32%. After removing the $$$ I got paid to do the 2020 Census, these are my percentages: 16% -5% -23% -26% 35% 43% -32% (month of August where I did the Census) -23% -27% -27% -6% -25%

In any case, I'm rambling.

I got an EIDL loan for $17,500 when I applied in August, so I never got the advance. If I understand the targeted program, $10,000 should hit my account once all is approved. If so, great! But, I wonder why they wouldn't just apply the $10,000 to my $17,500?

And when it rains, it pours... I applied for a PPP loan (first round) earlier this month and those funds just hit my account yesterday.I realize this is money that will need to be repaid. I'm using the money for legit purposes. These past 6 months have been the toughest and I've had to rely on credit cards to make ends meet (credit cards with interest rates at 27 - 34% and I had to do one of those payday loans to pay rent for February at 324%!!! Trust me, I'm not happy about these decisions, but I was able to keep my credit score from tanking)

I'm probably sharing too much here, but if anyone can glean some helpful insight from my comment after visiting to your site, I'm happy

ronald.l.walter

Saturday 27th of March 2021

Thanks for sharing that. I think it could be helpful for folks looking for answers. You know, in tough times we make decisions that we look back on and think, I could have done something different. But it's easier to look back and figure them out with hindsight than to make the decisions well when it's all happening and when the world is crashing in. I got trapped in that payday loan thing many many years ago, and it is a real trap. I'm glad you were able to get out.

I think you are right. There was another comment from someone who they reached out to that also didn't get the advance. So I hope that means you'll be able to get that soon. It would make sense to apply it to your loan, but maybe they aren't doing that just so people have the option in case they need that cash shot in the arm. Then you have the choice.

Good luck with everything!

Rie

Wednesday 24th of March 2021

So I finally got the invitation email (I'm in the second group that received no previous advance $) and I submitted my application and then the IRS form through the portal...and clicked Submit. I'm hoping that was the correct thing to do? Do you have any update on yours? Did you get the additional $9000 yet?

ronald.l.walter

Saturday 27th of March 2021

I haven't been funded yet, but it might be my fault. I did the same thing, submitting the form through the portal, and then heard nothing. I go back in and the submit button is lit up, so I clicked it. So I'll have to see what happens.

Kelly L Hammack

Saturday 20th of March 2021

I received the email for the targeted EIDL advance however when i go to try to log in with my EIN or Social Security number it tells me that it does not match so i am unable to do assess the application. I have called the SBA 1-800-659-2955 repeatedly and they say they cant help me that i need to email SBA at TargetedAdvance@sba.gov i have done this repeatedly and still no response or help. What else might i possibly do?

ronald.l.walter

Saturday 27th of March 2021

Hi Kelly, I'm so sorry I missed your comment earlier. I wish I knew what to tell you to try. The problem is the SBA is so backlogged that it's hard getting answers at that email address. I've directed questions at that email and only get a canned response. My guess is there was a typo the first time around - although I can't imagine they would have funded you the first time with a typo - unless maybe they were just pushing them through so fast they didn't check things well? Only other thing I can think of is contact your congressperson - somehow you have to get a live person to look into your account and I've heard sometimes someone gets some action if they get a push from their representative.

Kebir. A

Friday 12th of March 2021

Can you use unemployment benefits received if that is all you have for income? Thanks

ronald.l.walter

Tuesday 16th of March 2021

I don't believe that unemployment benefits are considered business income. Generally as an individual or independent contractor they're going off your Schedule C. Unemployment doesn't get reported on that (which is a good thing, you don't want to pay self employment tax on that).