Editor’s note: This was originally written about applying for the original advances/grants/loans related to the EIDL under the CARES Act of 2020. In July, 2020, funding for the advances expired. On December 27, 2020 a new stimulus was signed into law renewing features of the EIDL program. Many things remain the same as in this article, however there are some new qualifications. Read more about what is the same and what is changed under the new EIDL Grants/Advances/Loans and how it relates to sole proprietors or self employed independent contractors in the gig economy contracting with companies like Uber Eats, Doordash, Lyft, Grubhub, Instacart and others.

I looked all over for a step by step guide to filling out the EIDL (Economic Impact Disaster Loan) Application from the SBA as it would apply to independent contractors such as for Grubhub, Doordash, Uber Eats, Postmates, Lyft or other gig companies.

There’s a lot out there to help other businesses but something that walks through each step for contractors is harder to find.

So, I decided it would make sense to walk through the application myself and see what it was like.

Understanding the EIDL Loan/Grant and How it applies to independent contractors.

There were three facets of the CARES Act that were meant to help businesses as a result of the COVID-19 Corona-virus pandemic. Independent contractors and sole proprietors are eligible to apply for that relief:

- Pandemic Unemployment Assistance (PUA) . Normally self employed individuals are not eligible for unemployment benefits, however special provisions under the CARES act do allow contractors and sole proprietors to apply.

- Paycheck Protection Program (PPP). This is a forgivable loan created to help businesses maintain payroll. Independent contractors can apply based on replacement of owner income, though loan forgiveness is generally limited to about 75% of the loan amount for most driving-based gig contractors.

- Economic Injury Disaster Loan (EIDL). The EIDL was created to help businesses cover other business costs (not covered by the PPP). This is a loan with very limited loan forgiveness ($1,000 for the sole proprietor, $1,000 per employee up to $10,000 for businesses with employees).

Are contractors for Grubhub, Uber Eats, Doordash, Postmates, Lyft and other gig economy apps eligible for the EIDL Grant?

Yes.

The very first section of the SBA EIDL Loan application lists the types of businesses that are eligible. One of those options (the ones we would select if applying reads:

Applicant is an individual who operates under a sole proprietorship, with or without employees, or as an independent contractor.

Line 3 of income eligibility verification portion of the SBA EIDL Loan application

What can independent contractors use the money for?

Here are the regulations about what businesses can use the EIDL proceeds for, according to this article in JDSupra:

- Working capital necessary to carry the business concern until the business resumes normal operations, and

- Expenditures necessary to alleviate the specific econmic injury, which cannot exceed that which the business could have provided had the injury not occured.

The same article points out that the money can NOT be used to:

- Refinance long term debt that was incurred before the pandemic

- Make payments on federal loans (such as SBA loans)

- Pay for any outstanding tax penalties and fines

- Repair any physical damage to business property

- Pay dividends to business owners other than reasonable payment directly related to how they perform services for the business

In other words, it’s not meant to be free money, as a lot of people put it.

Is there really a $10,000 grant?

There is, if you have ten employees. As an independent contractor without employees, you are limited to $1,000 of the total loan that can be forgiven.

Can you take the EIDL loan AND The PPP Loan?

Both loans can be taken. The stipulation is that you can’t use it for the same thing.

As independent contractors the main use of the PPP loan is for owner income replacement. You wouldn’t be able to use the EIDL Loan for the same thing.

In other words you need to use the funds for qualifying purposes other than simply owner income replacement.

One thing you have to keep in mind: If you receive both the Paycheck Protection Program loan and you get the $1,000 EIDL grant, $1,000 of your Paycheck Protection Program would not be forgiven.

That really ends up making the $1,000 grant useless. It actually becomes a loan, but paid back to your Paycheck Protection Program loan payment.

I know, it’s weird. Welcome to the US Government.

Should you apply for the EIDL loan as an independent contractor with Grubhub, Doordash, Postmates, Uber Eats, Lyft or any others?

I can’t really tell you.

The bottom line is, you have to ask the question: was your ability to earn harmed by this pandemic?

For a lot of us in the delivery world, we’ve been making more than ever before. If you felt it was safer to stay home, that might be a different story. If you were in rideshare or some other field that was more impacted, you may be in more need.

In the end that’s a decision you have to make. Remember the ultimate purpose of this is to help those whose ability to earn was impacted by the pandemic and the shutdown of the economy and all that entails.

Here’s a couple thoughts I have:

You’ll need to keep good records of how you use the money.

Considering EIDL?

Get serious about treating your delivery work as a business. You need to keep good records.

If you don’t have a book keeping program or app, look into Hurdlr with free and paid options. One of the best mileage and expense trackers on the market.

There are a lot more specifics related to what you can and cannot use the money for. At the same time, it’s incredibly vague. Odds are, you could be having to do some reporting of how you used the money. There’s not a lot of detail out there that I can find on how that works.

At the same time, I wonder how much they’ll be able to put into checking out the details for every single contractor who took this loan.

Remember that this is a loan.

Do not confuse this with the Paycheck Protection Program. A substantial portion of that loan can be forgiven. This is not true of the EIDL. Forgiveness is essentially limited to the $1,000. The rest you’ll have to pay back and a 3.75% interest.

That’s a great interest rate compared to a lot of debts you may have. However, depending on how tightly they watch how you use the money, remember that one of the stipulations is you can’t use this to pay off existing loans.

I think our particular situation really complicates things.

Here’s one thing I love about independent contractor gig work like delivering for Uber Eats, Grubhub, Doordash, Postmates and others: It’s such a low risk low cost way to start a business. That’s even true with Lyft and Uber.

We don’t have any overhead related to the business other than our vehicles. Because most of us use our personal vehicles, that fuzzies the line between personal and business expense. Car payments and insurance and such are going to be expenses whether you are doing delivery or not. The substantial costs of doing business happen when we’re out doing deliveries.

But if we’re not delivering, we’re not running up those mileage based costs. If this loan is meant to cover business costs and we don’t have those costs, how does that work? And if we DO have those costs, does that mean we aren’t really economically injured by this whole thing? Do you see the catch 22 in all that?

I believe that for small operators like ourselves, it isn’t going to be an issue. Unfortunately, there’s so little actual guidance on this that I don’t know.

In the end, you have to make the call

I went through the application process just to experience the process. If I do receive funds, I’m planning to repay those right away, just to avoid any issues.

You’ll have to think through all those questions and make your own decisions.

Step by Step process to apply for the EIDL as a contractor delivering with Grubhub Doordash Uber Eats Postmates etc.

The SBA actually streamlined the application process. Parts of their application process in the past were related to identifying you are in an area impacted by a disaster. Since this is a nationwide thing, they took a lot of that out of their normal application process. I think part of it is too, they want to make it easier for people to start the process, and to quickly get the up-front grants ($1,000 to $10,000 depending on if you have employees) in the hands of business owners.

For the most part, the application is simple. There are a few parts that might trip up an independent contractor, since a lot of the language is built around business ownership. I’ll make an effort to highlight things that I think might be a stumbling point in bold colored type like this.

Step 1: Start the application.

That’s kind of obvious, isn’t it?

Go to the SBA application site for application. Do NOT go anywhere else – if it’s not on the sba.gov site, you’re in the wrong place. This is different than the PPP loan application where you apply through other lenders. You will apply directly with the Small Business Administration (SBA).

Understand: the steps that I walked through were as a sole proprietor as an independent contractor delivering for Grubhub, Doordash, Postmates, and Uber Eats. If you registered as a business entity (as an LLC or other form of incorporation) things may be a little different.

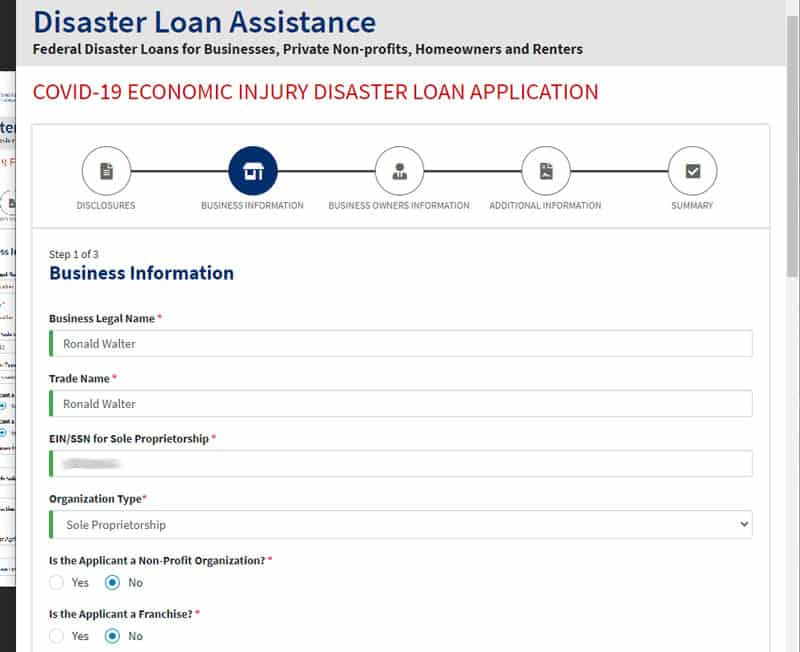

Choose one in the top section. I marked the third choice, as an individual who operates under a sole proprietorship. Then you need to go through, read, and check off each of the statements on the lower section.

When you do this, be honest on each one. When you submit this you agree that you’re telling the truth, under penalty of perjury.

Step two: enter your business information.

The first thing you do is enter YOUR business name. If you are a sole proprietor, that is YOUR name. Do not, I repeat, DO NOT put Grubhub or Doordash or any other company down for the business name. This is where you enter YOUR business name. If you are an independent contractor who has not set up a corporation or an LLC and you do not have an EIN (Employer Identification Number) you enter the name that goes on your tax form – which is YOUR NAME.

For the trade name I put my name in there. That’s because I haven’t established any kind of DBA or official business name. Most of us will do the same thing here. For the EIS/SSN you’re going to put your social security number. You will NOT put any information in here about any of the gig companies because, remember, this is about YOUR business, not theirs. If you have not incorporated you’re going to put Sole Proprietor as the business type. This is not a franchise operation and not a 501(c)(3) nonprofit operation so you’ll put no on both of those questions.

Step 3: Basic Financial Information for your business

The EIDL grant is very different than the PPP application in that you’re putting information in based on the 12 months before the event that happened. It’s not based on your Schedule C or annual taxes here.

And for those of us doing delivery, the only part that really applies is the gross revenue (top question) and maybe the compensation from other sources received as a result of the disaster.

Gross revenue received for the Twelve Months prior to the date of the disaster

You can’t get this off a tax form.

That’s because this is asking for your gross income earned from February 1, 2019 through January 31, 2020.

Now what makes this confusing is, when you apply for other aid, it’s usually asking for net (meaning what’s left over) and it’s usually asking for the calendar year. To fill this out, you need to add up all the payments you received from all the gig companies between February 1 of last year through January 31 of this year.

If you’ve been keeping track through a book keeping program like Quickbooks Self Employed (affiliate link – see the link in the footer for more information on my use of affiliates) it’s pretty easy, you just run a report. If not, you’ll need to go through bank statements and add it up. You can get reports from Grubhub and Uber Eats, but Doordash doesn’t make that information available going far enough back.

Add up all the money that came in from the gig companies during that time. Do not add up expenses or mileage for this.

Here’s the thing: If you’re going to go after this loan, you want to make sure you’re keeping good records. Find some kind of book keeping program, whether Quickbooks or something else, in the event that you need to provide reports later on down the line.

Cost of goods sold, rental properties and non-profit/agricultural income will generally stay blank.

Unless of course you are engaged in those opportunities. If you are buying and selling items, the cost of goods sold would apply. But remember this is generally about contracting with gig companies. For normal delivery operations you’re probably not going to have a cost of goods sold.

If you received other pandemic relief, you will want to fill out the “Compensation from other sources” line.

For example, if you applied for the Paycheck Protection Program, you’ll put the loan amount in here. If you received PUA (Pandemic Unemployment Assistance) you’ll enter this here. Then in the brief description section, enter the description of the aid you entered.

DO NOT skip this if you received any aid. If you received ANY form of assistance, you MUST enter it here. Failure to do so could create big issues.

Step 4: More business information

Okay, you could still call this part of step 3. I just couldn’t fit the whole page into a screenshot, so I’m going to call it step 4.

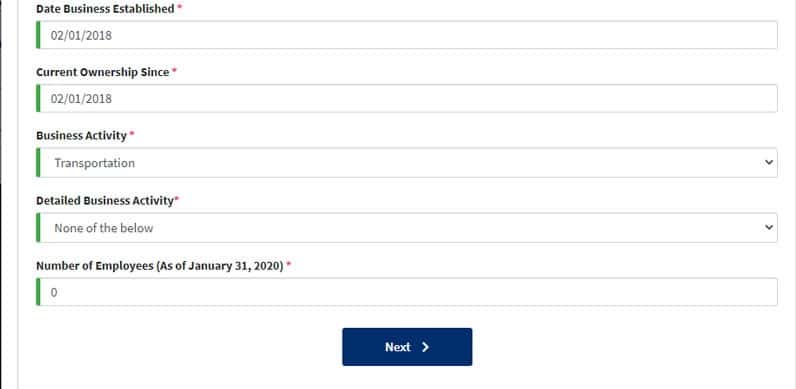

You want to think about this in terms of how you’ve done independent contractor or gig work in the past. When did you start doing work that you would report with 1099’s and a Schedule C? Has it all been on ONE schedule C? Use the start date for that as your “date business established.”

For example, I first started taking delivery work in February 2018. I had done some other self employed work prior to that but it was a different style of business. I also have a separate business for my website because it’s substantially different. In my situation, I use a different Schedule C for that. However, my primary business has been delivery, so I’m using the February 1 start date.

With gig work, it’s pretty rare that you would buy the business from someone else, so generally your “Current Ownership” date is going to be the same as the business start date.

Business activity

Here’s where you classify what kind of business you are operating.

Transportation was the closest match I could find. I went through each category in the dropdown and nothing seemed any closer.

I also chose Transportation because of the category that best fits us when filing your Schedule C as a contractor for Grubhub, Uber Eats, Doordash and others. On line B, the best fit I found is “Transportation and Warehousing” and then the option 492000 Couriers and Messengers is the sub category.

When you select Transportation on the EIDL loan, there really isn’t an appropriate sub category, so I selected “None of the Below.”

Number of employees

I have that title in bold and in red because this is one that trips a lot of people up.

You have no employees.

0

None

I know it’s tricky. We think that we’re self employed so that means we have one employee.

But here’s the thing. We don’t run payroll. We don’t do all the payroll things on ourselves. Not unless you’ve incorporated. As an independent contractor, you enter 0 as in zero.

You can confirm that in this article by Gusto, a payroll processing company.

Step 5: Business owner information

This is pretty simple: You enter the relevant information about your business owner (who happens to be you).

If you have a partnership or corporation with several owners (rare when doing gig work) you can fill out a separate form for each owner. I don’t think this is too complicated. Owner is the best title to use and for most of us as independent contractors, we’d enter 100%.

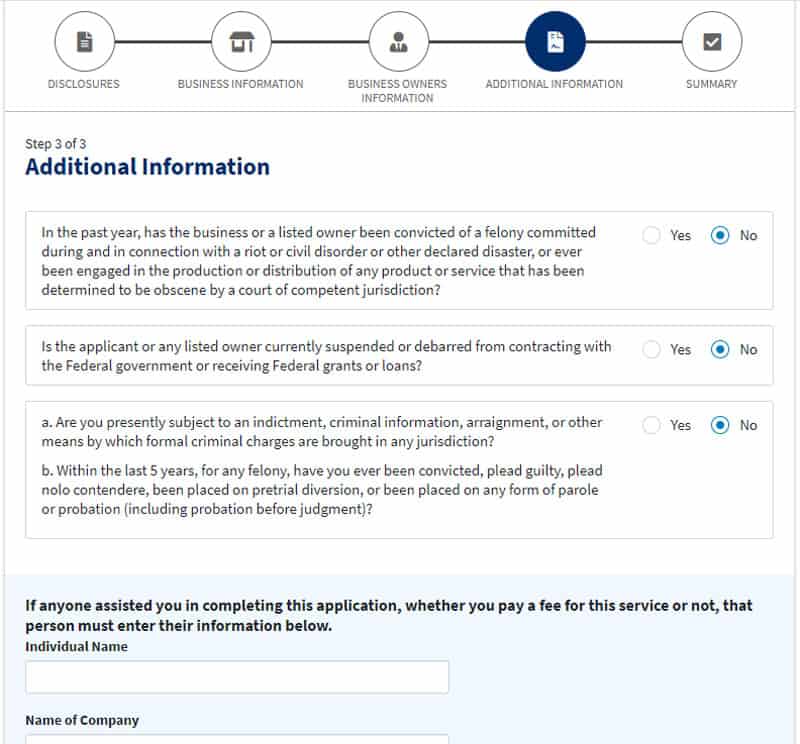

Step 6: Additional information

This section is pretty straight forward. It’s asking about your criminal history. It goes into questions about if you’ve been banned from getting federal aid or contracting with the federal government. Then it gets into if you have any felonies or if you have criminal charges pending against you.

After this, it’s asking if anyone assisted you in completing the application. This is where you had someone like an accountant or professional put this together for you. If you did, you’re probably going to know it and they’re probably going to advise you to say yes. Otherwise, you’ll probably leave this blank.

Step 7: Bank info

If you want the forgivable grant, check the box!!! The grant part of this whole EIDL Loan/Grant thing is the advance. Make sure you check the box!!! (I know, multiple colors are annoying but I’m trying to get a point across).

The $10,000 amount is confusing. Some are mistaking that for you saying you want to borrow the full $10,000. That’s not what this is. This box is asking if you want to receive an immediate advance (for independent contractors with no employees, that’s $1,000).

*** Edited – as of 7/17/2020 *** I received a couple of comments recently that the check box is missing. I did find out that the box is no longer there. Looking into this, I found that the reason it has disappeared is that the advance grant of $1,000 is no longer available (or of up to $10,000 if you have employees). It appears that around the 13th, funds have run out for the grant portion of this aid.

This is the part where you get the $1,000 that doesn’t have to be repaid (unless you are getting loan forgiveness on PPP). The SBA will follow up later to talk about loan amounts. If you want the grant portion, check the box.

The rest is pretty straight forward. Bank name, account number and routing number.

Again: make sure you are on the sba.gov site. Don’t enter this information if you’re not absolutely sure.

You need to have some kind of place to have direct deposit. If you don’t have a bank account, perhaps you have a debit card like what GoBank (provided by Uber) uses. Check with your debit card provider and see if they provide a routing number and bank account.

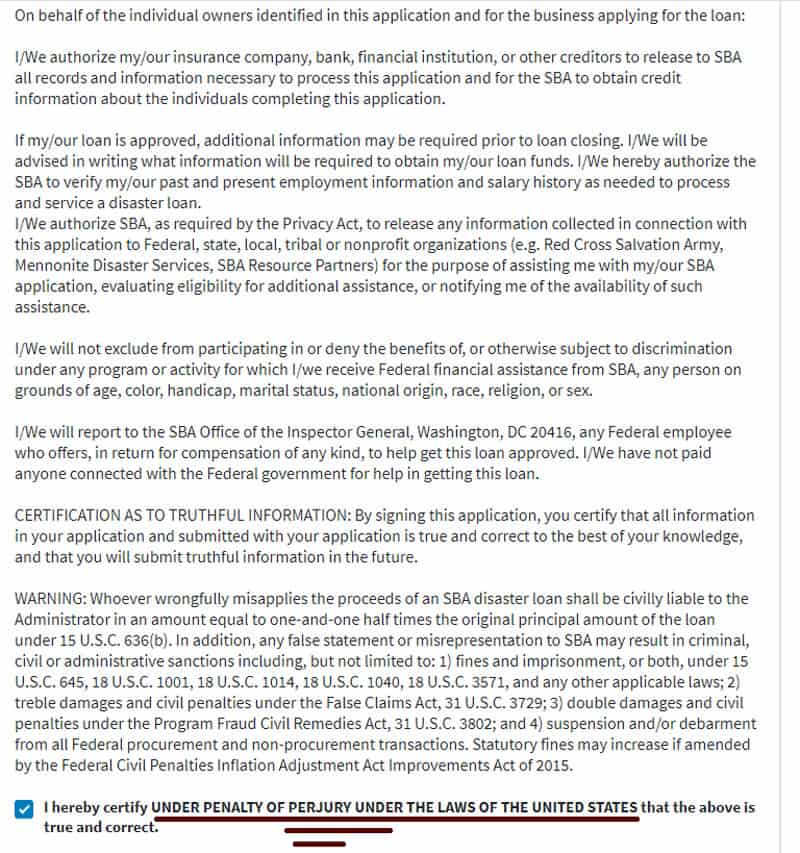

Step 8: Pinkie Swear

Here’s where you’re stating that you’re telling the truth. You’re also agreeing to some things.

Read this. Seriously, if you’re going to check it off, read it. Remember that this is a business loan and you need to take it seriously like a business transaction. Too many contractors sign up with these gigs without paying attention to what they’re signing up for.

Don’t do this here.

Here’s a couple highlights: You’re agreeing to let them check you out. That means they can check your taxes or insurance or banking. You’re agreeing to let them share information. Be careful about this, don’t try to fluff up your income to get more money here and think the IRS can’t find out about it.

And you’re saying you are telling the truth. You’re agreeing that you can be charged with perjury if found to be lying.

For most people reading this, none of this is an issue. Just… make sure it’s not an issue for you.

And that’s about it.

It’s not a hard application. Just remember that unless you’ve incorporated (and I’m guessing you’d know if you did) you’re applying as you, not as Grubhub or Doordash or Uber Eats or anyone else. As a sole proprietor your business is you.

I’ve read up on a lot of things about what happens next. The problem is that a lot of what I read was different than what I experienced. So I’m not going to share any of that just because I’m not sure how much things have changed since they wrote whatever they wrote.

What I’ve heard is that the advance is sent almost right away. That’s the part that you won’t have to pay back (unless you’ve already had your PPP loan forgiven – my understanding is you can’t have that fully forgiven AND this $1,000) At some point you’ll find out if you’re approved or denied for a loan, you can choose whether to accept the loan or not. They may ask for more information or for tax documents.

I’ll post again as things happen for me and let you know how it went on my end.

To be honest, I’m hesitant about applying for this. When I started writing about the PPP there was a lot of information missing on how things work with independent contractors. That’s nothing compared to the information available here. The SBA doesn’t have any solid instructions on how to answer these questions (not that I could find). Not like they do with the PPP, and definitely not like you find with tax forms.

That’s why I may just reject the loan altogether. For me this is more about learning the process to try to help people. I don’t have a lot of information on how you’re supposed to track what you spend – in fact I have none.

This can be an option for some emergency cash to get you by. That said, I advise caution. But in the end, you have to decide what is best for your delivery business.

Kifach

Wednesday 22nd of July 2020

Hi,there is anyway how to return the money back?i got 45k $,and I don’t really need it if I can’t use it for something else.i am Uber drive

ronald.l.walter

Thursday 23rd of July 2020

You can definitely just pay it back.

I'm pretty sure they would have had you set up an online account for the loan. You should be able to find instructions there on how to pay it back.

If you can't find anything there, I did find this link: https://aksbdc.org/2020/06/returning-eidl-procedure/. T

Shervin Firouz

Wednesday 15th of July 2020

I followed everything but I still dont see the checkbox for the advanced grant anywhere.

Tabitha Miller

Friday 17th of July 2020

I can't find the check box either!

Demetria

Sunday 12th of July 2020

I heard there was a $3,000 Grant. But after reading your article, is it really just a small contractor loan?

ronald.l.walter

Wednesday 15th of July 2020

There are so many reports out there, it's hard to keep them straight. Even the government can't always get them straight.

The way I understand it, the original legislation intended it to be a $10,000 grant across the board. But then SBA interpreted it as UP TO $10,000, basing it on $1,000 per employee up to 10 employees. So based on their rules, we only get the $1,000 grant.

My guess is the $3,000 grant number came from either someone who had a total of three people, so they got the $3,000. OR they got the Paycheck Protection Program loan which varies based on your taxable profits from last year.

Connie

Thursday 2nd of July 2020

I agree. “Cost of goods sold” is as concrete as it sounds. I was just trying to cover my bases should IRS or SBA question anything about my reporting to one versus the other not being consistent. But of course, it will be since I’ll be reporting the same gross revenue and no cost of goods sold for each reporting. It will be my first year not filing as simply a w-2 employee, so independent contractor/ self-employment filing requirements/tax laws are very new to me. I think that in my overwhelmed state of mind, I just confused myself. Thanks so much!

SHERIEE NYANDEH

Thursday 2nd of July 2020

My husband and I started a homebased business 11/01/19. We established it as a LLC and have a EIN# and business bank account. When attempting to apply for the $1000.00 grant the system indicated to remove the second company owner. I own 60% and my husband owns 40% of the business. What do I need to do ? Thank you, Sheriee N.

ronald.l.walter

Friday 3rd of July 2020

Hi Sheriee

I don't know enough about the inner workings to give you an authoritative answer, but I'll throw out some guesses.

My first thought is to wonder if you chose sole proprietor on the initial page of the application or under the business type. There may be a setting in their application that won't allow you to enter more than one owner's information.

I'm guessing you may have done this already, but my first thought would be to double check that on the first page of the application and make sure you chose the top option instead of the sole proprietorship - so for you since you are registered as an LLC I would expect the "Applicant is a business with not more than 500 employees." And then under the "Organization type" in the Business Information section make sure you've selected Limited Liability Corporation.

If those are entered correctly, I'm not sure what to tell you from there. Did you have someone help you set up the LLC? Maybe double check with them and see how well they understand the application process, they might know more about that aspect of things than I do.

Okay, a lot of people know more about a lot of aspects of this whole thing than I do.