You may have found out that personal insurance policies generally do not cover delivery driving for gig companies like Grubhub, Postmates, Doordash or Uber Eats, so how do you find the right insurance?

Do you have to get commercial insurance? Is commercial insurance too expensive? Are there other options? Is there a chance your personal insurance DOES cover you?

It’s important that you make sure you have the proper insurance. Most personal policies specifically exclude commercial use of your vehicle, delivery work, or livery (transporting goods or people for hire). That means you are not covered if there is an accident on delivery. Grubhub does not provide any kind of insurance. Doordash and Postmates have liability insurance policies that may cover damage to the other party but have no coverage for you or your vehicle. Therefore, you are taking a tremendous risk if you don’t make sure you have the right insurance.

How to get the right insurance as a delivery driver for Grubhub, Doordash, Postmates and others: Three Steps

Let me be clear here: I’m not a fan of how insurance companies work. In fact one of the reasons I’m adamant about making sure you have the right insurance is, I know they will do everything they can to avoid paying out. Don’t give them a ready made excuse.

Some will tell you to go right away to commercial insurance. You may need to – that is the route I went, however there may be better options for you. Here are the steps I recommend:

1: Check your policy

Ready to get bored? Woohooo! Here we go! Read your policy.

Not the most exciting thing you can do, right? It might be easiest if you have access to your policy in a PDF format. That allows you to do a search. For most policies, the place you want to look is anywhere that has exclusions. In fact, you can search for terms like “Exclusions” and if you have a heading in your policy that says “Exclusions, read through those to see if anything applies to delivery. Search for things like “delivery” “commercial” or “livery.” Look for any exclusions that might refer to anything like commercial use or livery (“livery” is a term for the “transportation of goods or people for hire.” Delivery for gig companies is considered livery work).

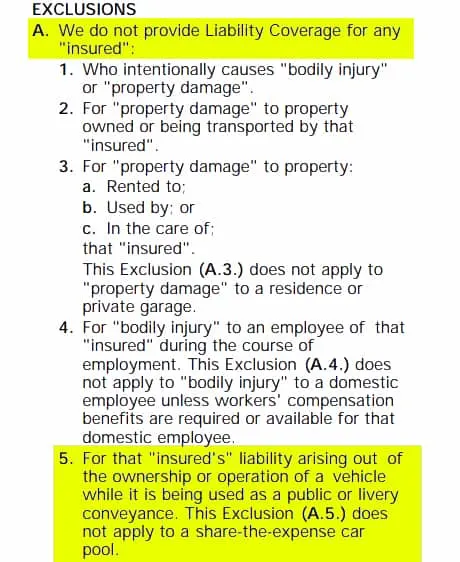

Here’s an example. In this particular policy, there were exclusions like this under all the different types of coverage. They excluded these things from liability coverage, comprehensive and collision and even bodily injury.

Call your insurance company for verification.

If you were not able to find the exclusion, do not assume you are covered. There may be other language somewhere that you weren’t able to find. If you contact your agent or contact the call center for your insurance company directly, they should be able to clarify if you are covered. Perhaps use language like this: “I’m considering earning some extra money as a delivery contractor and I want to find out if my insurance covers this type of work.”

If they say yes or no, ask them what language in your policy either excludes or allows the delivery work. Be careful here – I’ve heard of some agents who were misinformed on this, that’s why the clarification is important. If they insist that you are covered, ask them if they can send you an email or send you something in writing to confirm this. You want to have documentation.

There are some policies that you might be okay. If you have verified everything is okay, you’re in the best possible spot. You don’t need to look further.

2: Ask if there is an endorsement or rider available for your policy to allow delivery.

Your next best scenario is if you can get an add on to your existing policy that will cover you while on delivery. Some insurance policies do this, some don’t. I have a summary of insurance from my personal policy (for my wife’s car) that says ” Unless you have purchased the appropriate endorsement, your policy excludes coverage for livery conveyance. If you are a driver for a transportation network company, please verify you have purchased appropriate coverage” I found it interesting that they said this because they didn’t offer such an endorsement.

While you are on the phone with your insurance company, ask them if there are any endorsements or riders available. You might ask if they have a rideshare option, and does that rideshare option provide coverage for delivery work.

Some rideshare policies will NOT cover you. The reason is that they rely on the coverage provided by the rideshare company (Uber or Lyft), where their insurance is assuming most of the risk. Such rideshare policies only fill in the gap. However, with companies like Doordash, Postmates, and Grubhub, they do not provide the kind of insurance that Uber and Lyft do, and what this does is shifts the entirety of the risk to the rideshare policy. For that reason, many rideshare policies won’t cover delivery.

The extra cost for such an endorsement or rider is probably lower than a commercial policy. If that’s available, you’re probably good. However, it doesn’t hurt to check into other options.

3: Start Shopping.

If you cannot get the coverage you need, you need to either look into getting another policy, or closing up shop on your delivery business. Do NOT continue to deliver while not being covered.

There are two places you can go. Other personal policies that might cover you, or get a commercial policy.

Search for personal policies

My first piece of advice here is don’t assume that because an insurance company comes up when you google car insurance for delivery drivers, that it means they PROVIDE that insurance. I’ve seen too many cases where companies show up in those searches that do not provide insurance.

Out of curiosity, I went through the quote process for Root Insurance. I couldn’t get anyone to answer the question straight up as to whether they cover delivery work. With them, you have to go through a several day process of having their app evaluate your driving before they give you a quote. The rate was awesome when they finally gave me a quote. Unfortunately, it was at that time that I could finally talk with someone and ask specifically about delivery. Any quote you get, you have to ask them specifically if delivery work is covered.

Your best route might be to get with an independent insurance agent. Find an agent that represents several companies. They can do the searching for you. They may have options for commercial insurance as well.

Check specifically with companies that are more likely to provide coverage for delivery.

I am hearing that State Farm is one of the most likely to provide delivery coverage. I’ve also heard that Farmers and Allstate may as well. Understand though that coverage by each company differs by state. That’s why it’s important to verify that the company does cover you when you get a quote.

Check into commercial insurance.

Commercial insurance that is designed for on demand work like ours isn’t always that much more than a personal policy. Two years ago I signed on with Geico Commercial and they weren’t that bad. Geico and Progressive are two that have commercial divisions. Do not confuse either of them with their normal insurance. Their commercial insurance divisions work separate of their consumer insurance.

I have two options that might make it easier to check multiple options. You may have seen ads on the site for Tivly. Full disclosure: Some links are affiliate links, meaning commissions from them helps keep this website active.

You can always search individual companies. In some states it may be harder to find good options than others. I tend to like having options available where someone else can do the work for me, you know? That’s why I would lean towards using an independent agent locally as the second option, or searching one of these options above.

Getting the right insurance is an important business decision.

Do not make the mistake of delivering if your insurance doesn’t cover you. A driver in Northern Colorado is looking at possible bankruptcy now because her insurance won’t cover damage to her car or the other person’s car since she was on delivery. Do NOT make this mistake.

I hear from people in some states where the cost of such insurance is prohibitive. I get that it doesn’t make sense to spend several hundred dollars a month to be able to do this work. If that’s your only option, this might not be the best business model for you. I would suggest it’s better to not do delivery at all than to be uninsured. Don’t take stupid chances.