Am I the only one disturbed by what’s going on with how some PPP lenders and agents are handling the Paycheck Protection Program? Especially in how they’re approaching it with gig workers and self-employed independent contractors?

We’re getting close to the PPP deadline (May 31, 2021).

On April 13th, I received an email from a lending agent telling me there’s only $54 billion left. One week later the same agent told me there’s $40 billion.

At that pace, funding won’t last beyond mid May.

And there’s a feeding frenzy going on. Lenders are swamped with last minute applicants. Banks and lending agents are flooding our emails and social media feeds urging us to apply.

Some things I see in the midst of this are bothering me. I don’t know if ethical lines are being crossed, but something just doesn’t pass the smell test.

There’s big money in processing PPP Loans.

It’s probably no surprise that there’s a reason everyone’s trying to get you to take the PPP.

If you get funded, other people are making money.

The SBA define the processing fees for lenders:

SBA will pay lenders fees, based on the balance of the financing outstanding at the time of disbursement of the loan, for processing PPP loans in the following amounts: For loans of not more than $50,000, an amount equal to the lesser of fifty (50) percent or $2,500).

SBA Interim Final Rule of January 2, 2021, page 68, section 5 and reinforced by the SBA Procedural Notice of February 8, 2021.

If the loan is $5,000 or less, the bank gets a processing fee for HALF the loan amount. If it’s more than that, the bank gets $2,500.

There are other formulas to calculate fees for larger loans. However, we’re focusing on self-employed individuals and independent contractors with gig companies like Doordash, Uber Eats, Grubhub, Instacart, Uber and Lyft who won’t have loans that high.

One of the things the government wanted to do when they re-introduced the PPP in December was to get more money into the hands of smaller business owners and independent contractors. The Biden administration reinforced that priority when they 1) allowed more contractors to qualify and 2) allowed the self-employed to receive funding based on gross revenue rather than net profit.

In fact, processing fees for the first wave of PPP loans in 2020 were only 5%. Instead of $2500, a lender only received $250 for a $5,000 PPP loan.

All of a sudden the financial incentive for processing loans for self-employed independent contractors got much higher.

The trickle down of PPP processing fees.

Paycheck Protection Program loans are not processed directly by the SBA, but are processed instead by banks and other lenders. Registered agents often do the marketing and bring applicants to the lenders in return for a piece of the processing fee. Womply is an example of such agents.

It makes sense. It seems only fair to give agents a piece of the action in return for bringing applicants in.

Somewhere along the line agents figured something out. It costs less to pay others to find applicants than the marketing cost to find the applicants themselves.

To this day I’m thankful for one thing about Womply. Most lenders weren’t very interested in the self-employed. Conversely, Womply was among the first to really provide information on how the PPP worked for independent contractors and to try to make the process easier for them.

They were smart enough to partner with content creators like myself. They then realized the value of word of mouth, and started offering referral fees.

And then it got crazy.

In February, they offered a $20 referral fee. By March they were bumping referrals up to $200. Delivery driver forums and groups were swamped with people throwing out their referral codes. Suddenly, PPP was all anyone could talk about.

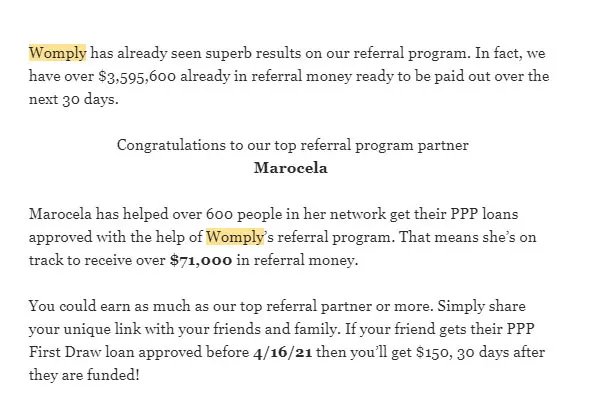

Womply recently sent an email offering results of their referral program. One person was on track for $71,000 in referral money.

Seventy. One. Thousand. Dollars.

That’s a lot of referral money.

The thing is, if an agent is paying out $71,000 to one person for referrals, you can guess how much money that agent is getting themselves.

So what do I find questionable about all this?

Actually, nothing so far. I don’t have a problem with the referral fee and application fee system.

The SBA was very clear they wanted to get more money to small businesses and especially to self-employed folks. This interview with one of the top SBA officials is an example. The legislation dramatically increased the incentive for lenders to work with smaller loans.

All of this did exactly what it was intended to do. It got people into the pipeline. My observations in forums and groups for Doordash, Uber Eats, Grubhub, and other gig drivers was that the PPP was largely ignored earlier in 2020. However, by the end of March, PPP was a dominant topic.

I think the part that’s making me uncomfortable has to do with how I’ve seen some things change in the application process. It has felt to me like the focus has shifted from truly helping independent contractors to figuring out how to cram as many applications through without regard to if a person qualifies.

Why would they do that? Because there’s good money in getting someone funded. It doesn’t matter if they actually qualify. There doesn’t seem to be any concern about if someone can have the funds forgiven. All that matters is getting people funded.

I can’t tell you if this is the actual motive for any of these companies. I can’t get in the heads of the decision makers and read their minds.

But what I can tell you is, if you get funded, they get paid. Handsomely.

Here are a couple of things that I have observed that make me concerned.

1. De-emphasizing qualification.

The thing about the Paycheck Protection Program is, there’s a short amount of time to get millions of applications processed and funded.

Normally, when you get a loan from the SBA there are a LOT of steps involved. The lender has to verify a lot of things. The SBA has to verify things. Several steps are involved. It’s tedious and time consuming.

Multiply that times millions of applicants and you can see how this can be a problem.

Legislation and rules for processing the PPP changed, especially after December, to make the process easier. In a nutshell, the SBA said lenders don’t have to verify documentation. They can accept the applicant at their word.

The lender does not need to independently verify the borrower’s reported information if the borrower submits the documentation supporting its request for loan forgiveness and attests that it accurately verified the payments for eligible costs.

SBA PPP Interim Final Rules, January 2, 2021, page 68 item 5.

As a result, I’m seeing more people get funded who didn’t qualify. For example, many have reported that they didn’t start delivery until after February 15, 2020 and yet received funding.

I don’t have an issue with people receiving funding even if they didn’t qualify. The problem I have is where it can impact them when they find out they have to give the money back.

The disappearance of the income qualification questions on 2nd draw applications.

With the reintroduction of the PPP, the second draw had some income qualifications. You have to document a 25% loss of income for at least one quarter compared to the previous year to qualify for the second round.

Shortly after the second draw was created, I wrote about how to apply, with a lot of screenshots. A significant part of the application was to identify that loss of income.

Things changed when Womply created their Fast Lane application.

There is much about the Fast Lane that I thought was brilliant. They streamlined the application and took out a lot of friction points that slowed things down for a lot of people.

I had an issue in my own application where the lender they sent me to was too overwhelmed to take me on. So, I had to go through the process again. The Fast Lane fixed that problem for future applicants because it gathered all the information needed, and then would submit it to a lender and take care of the whole application thing. It allowed a lot more people to get through the process.

They also added a piece where you could agree to have Womply submit a second draw application. Again, it was brilliant in streamlining the process. But one piece really raised a concern for me.

Where’s the income qualification portion in this screenshot?

There is none. Nothing in the application said anything about the 25% decrease. I asked someone from Womply, “If they choose the 2nd draw in addition to 1st draw, do they get a followup that requests their quarterly income (since that was part of the 2nd draw application to qualify under the loss of income stipulation)?”

The reply I received: “Not with Fast Lane. The documents required for Fast Lane are their 2019 1040 and Schedule C or Schedule F.” I followed up to clarify why that wasn’t in there, and was told it was up to the applicants to certify or acknowledge they qualify. No documentation was needed.

The problem with no longer addressing income qualification.

Nowhere, anywhere in the application, is there anything about that income qualification. Even the followup screen ignores the issue.

I know this from discussions in online groups and forums that a lot of people think they’re getting the second draw and they believe it will be forgiven.

Nothing in the process here tells them otherwise.

I understand that it’s the responsibility of the person applying to know what they’re eligible for and what they aren’t. I get that completely. That’s why I’ve written so many articles on the PPP, especially on whether you qualify for the second draw. You should know that.

But we all know how it is with a lot of gig workers. Drivers for Doordash, Uber Eats, Grubhub, Instacart, Uber, Lyft and other gig platforms aren’t always doing that. They often don’t exactly treat this like a business. They should.

Related: One big problem with pushing applications through with so little vetting and documentation is that it opens the door to PPP Loan Fraud – read more here.

I mentioned how they took away some of the friction when they streamlined things with the Fast Lane. It just seems like this is one of those things. If you don’t qualify, you won’t apply. If you don’t apply, they don’t get paid. So instead, let’s not talk about whether you qualify and just have you apply anyway.

Taking the qualification questions away means more are going to apply thinking they qualify. And if they think they qualify, they think they’ll be able to get it forgiven. They’ll get a rude surprise when they won’t get the loan forgiven.

But hey, as long as the loan is funded, Womply and the lender all get their money. That’s what matters, right?

2. Pushing through promissory notes to applicants who didn’t apply.

I’m hearing people who are getting promissory notes on their second draw loans. The problem? They never asked to apply for the second draw.

And again, this is being sent to people without regard to if they meet the income qualification (and without even being asked if they do qualify).

I know one person who told me they very specifically asked for only the first draw, because they knew they didn’t qualify for the income reduction piece. Yet the agent they used is still sending them a promissory note to get funded for a second draw PPP loan.

I just have a problem with any approach that says hey, we took the liberty of getting you approved for a loan that you didn’t apply for. I don’t know what the professional ethics are around that, whether it violates any industry code. Just as a lay person observing from the side, it seems shady.

3. A lack of interest in whether folks get the loan forgiven.

A hot topic in the driver community has been, what do we do with the money now so we make sure it gets forgiven.

I asked a contact about this. I wanted to put together information about how The short simple reply? “No one’s talking about forgiveness.”

I get it on the one side. Lenders and agents are overwhelmed with applications, trying to get funding through before that last $40 billion disappears. I’m sure that’s all that’s on anyone’s mind.

But in the end, I walk away with the feeling that loan forgiveness doesn’t matter here. All that matters is funding. If the loan isn’t forgiven, that’s no skin off their back. They got paid.

How can this be a problem for gig workers and other self-employed individuals?

The main thing is, it’s setting them up.

The system is designed right now to get applications pushed through in a hurry. There’s no real verification going on.

That doesn’t mean there won’t be verification. It will happen, when it’s time to apply for forgiveness. At that time, gig workers can expect to provide proof that they qualified for the loan. Many will discover they discover they never did qualify.

What happens then? Will they be require to pay the funds back immediately? Or will it just roll into a loan payment at the 1% interest. You would hope they have time to pay it back, but the reality is they certified something that wasn’t true. Where does that leave them?

Another issue that it creates is, these lenders and their agents have been pushing applications through without regard to whether someone qualifies. As mentioned earlier, funds are expected to run out before the end of the deadline. How many people who legitimately qualify are left out in the cold as a result?

It’s not that self-employed who get caught in this mess are without fault.

Maybe for some, this will be a wakeup call. I watch a lot of gig workers who deliver for Doordash, Grubhub, Uber Eats, Instacart, Postmates and others, or who do rideshare for Uber and Lyft, who have looked at this as a charity giveaway. The reality is it’s a business loan. There can be consequences to not taking it all serious.

In the end, it’s still the responsibility of the self-employed person to understand what they just said when they certified that they qualify. The reality is there are huge numbers who likely didn’t even pay attention to what they were clicking on when they certified that very thing.

Just give me the money.

That’s kind of the theme, isn’t it? I don’t care if the borrowers get forgiven, just give me the money. I don’t care what the document I just agreed to says, just give me the money.

What should independent contractors and self employed individuals do?

There are a few things.

First, educate yourself. Understand what the qualifications are. Especially for the second draw. Our article on how to apply for the second draw PPP loan isn’t nearly as streamlined as some of the applications out there.. We put some steps in there that go beyond just clicking buttons. They’re worth paying attention to in order to avoid future issues.

- Determine if you qualify. Understand how the 25% income qualification works.

- Get your finances together. Add up your income for each month of 2019 and 2020.

- Run your taxes for 2020. Your 2020 Schedule C can be very helpful here.

- Get your documents together. At some point you’ll need to show you qualified. Be prepared.

My opinion is, the way some of these lenders and agents are pushing applications through just seems shady. I hope I’m wrong, but I get the impression they don’t care if you qualify to have this loan forgiven. All that matters is getting as many people funded as possible.

They know a lot of self-employed people aren’t paying attention to whether they qualify. My suspicion is they don’t want them to. All that matters is people get funded. In that way I think they’re taking advantage of the sloppiness of the contractors and individuals who rush through this. It’s the same kind of thing as when Doordash, Uber Eats, Grubhub and others take advantage of independent contractors who don’t pay attention to what they’re signing up for.

That doesn’t absolve you of your responsibility. Pay attention to what you’re agreeing to. Furthermore, understand what you’re applying for. Take responsibility for yourself and you can’t be taken advantage of.