Three Steps to Understanding How to Verify Your Income as a Gig Economy Contractor

There are no paystubs when you are a self employed contractor for Grubhub, Uber Eats, Postmates, Doordash, Lyft, Instacart or other gig economy apps, so how do I verify my income if I want to rent an apartment, get a car loan or take out a mortgage?

Here’s the important thing to remember. You are not an employee of any of these companies. You cannot and will not get a paystub or W2, or anything like that.

That means you may not be able to get any kind of proof from them verifying they paid you anything. (I’m looking at you, Doordash). Does that mean you’re screwed when it comes to anything that requires income verification?

No. Not if you approach it right.

Read on for three steps you need to take to make sure you are properly presenting and verifying your income as a contractor for Doordash, Uber Eats, Grubhub, Lyft or any other gig economy apps.

But here’s what it boils down to:

You are presenting your information as a business owner. Not as an employee.

When you understand this one important fact, you’re in a better position to properly and successfully verify your income whether you’re applying for a loan, a mortgage, an apartment lease or anything similar.

Remember that you are not an employee.

When you are applying for a car loan, mortgage, apartment lease or something similar, do not go in stating you are an employee of Grubhub or Doordash or Uber Eats or any of these apps.

You are not an employee.

These companies are not your employers.

They are you CUSTOMERS.

That means you need to present your information not as an employee, but as a business owner.

Step 1: Understand What Your Business Income is.

The first step of being able to successfully verify your income from Doordash, Grubhub, Uber Eats, Lyft and other gig economy apps is to understand exactly what that income is.

Your income is NOT the money that comes from these gig companies. These lenders and creditors look at that money as your business revenue.

They also understand that a business has expenses. They want to know about those as well.

In other words, they want to know your profit. It’s important that they know both the income and the expenses, the profit and loss. They want to know how much is left over at the end of the day.

Since that’s what they want to know about, it’s a good idea to understand what profit and loss is all about.

Your business could be bringing in a million dollars. However, if it’s paying out a million and a half dollars, lenders aren’t very confident that you’ll be able to keep up with your loan or rent payments.

Step 2: Present your earnings by way of profit and loss.

Do not tell a lender or apartment management company that you are an employee of Doordash, Uber Eats, Grubhub or any of the gig companies.

That’s going to get you off on the wrong foot. That’s because the bottom line is, you can’t back it up. You have no paystubs and you won’t be able to get any documentation or letter from these companies confirming you are an employee.

THAT is because you aren’t an employee.

Why this is so important to understand

I know, I’m repeating myself a lot on this. I’m doing that because this is incredibly important for you to get it right from the beginning.

If you’re getting a loan, the lender is going to want to know they will get their money back. If you are renting an apartment, the owner or manager wants to know they’ll get their rent.

But here’s the thing. If you have a regular paycheck coming in, they’re a lot more comfortable. They know there’s a higher chance you’ll continue to have money coming in.

But once it’s from a business, they get a bit more nervous. There’s a higher risk that you may not be able to pay up.

So if you’re coming in, asking for a loan or committing to an apartment, and you don’t understand your status, that doesn’t do much to help their confidence.

You want to go into this understanding exactly who you are: A business owner and not an employee. And you want to go into your application in a way that is going to make them feel comfortable that you are COMPETENT as a business owner.

The best way to show competence as a business owner? Present your income by way of a profit and loss statement.

What’s a profit and loss statement?

If you’re asking this question, it’s a good thing you’re reading this. If you’re walking into a loan office or apartment complex saying “I want you to approve me based on my business income” and you don’t know what a profit and loss statement is, you may be in trouble.

You may have some experience already with a profit and loss statement. If you’ve filed taxes as an independent contractor, take a look at your Schedule C. Check out the title line: “Profit or Loss from Business.”

Profit and Loss Statement defined.

A profit and loss statement is a common report for businesses.

Very simply, it’s a statement that shows how much money has come in, and how much money went out.

I mentioned earlier that the money you get from Doordash, Grubhub, Uber Eats, Postmates, Lyft, Instacart or any other gig app is NOT your income. But it is your BUSINESS’S income. That goes in the income section of your profit and loss.

The second part of a profit and loss statement is your expenses.

In other words, it’s how much money you’ve spent for your business. What supplies did you need? What did it cost to operate your car?

You list all of your income sources, then you provide a categorized list of expenses. If you had money left over, that’s your income. If expenses were more than your income, that’s known as loss.

How to come up with a profit and loss statement.

Here’s the most important thing:

You need to keep good records. You have to.

Whether you are writing it all down by hand, or using a book keeping program, you’ve GOT to keep good records of what you’re doing.

You can try out programs like Hurdlr or Quickbooks Self Employed.

Hurdlr has a free program that works great for tracking mileage, income and expenses (referral link). There is also a paid version that has more advanced reporting and automatic tracking.

In my review of the best gps mileage and expense tracking apps, Hurdlr came out as the top overall pick.

This is a referral link to Quickbooks Self Employed, a better known program. (I may receive compensation if you purchase from it) You can also read my review of Quickbooks Self Employed and how it works for independent contractors in the gig economy

Here’s the thing to consider: Using a program like this gives you an air of legitimacy as a business owner. If you keep up with your records and can pull up a P&L (Profit and Loss) report, it communicates to the people you’re applying with that you’re serious about what you are doing.

You can create your own Profit and Loss Statement.

If you’re not using a program, you can still create your own P&L.

If you’re not sure how to structure it, a good guide would be to use the expense categories used on your Schedule C from your last tax return. Add everything up in each area for the year to date as though you were running your taxes.

If you have not filed a Schedule C, you can read more about it on this article we put together as part of our tax guide.

If you fill out your own, here’s what I would recommend:

In the income section, break down your income.

What is the total you received from Grubhub, from Doordash, from Uber Eats, etc.? Obviously if you only work with one, that won’t matter as much.

Here’s the thing about record keeping: You should be tracking all that yourself. You may or may not be able to get the totals from each of the apps but you should already what you earned from each.

Then create a new section for expenses.

Break down your expenses by category and add the totals up for each.

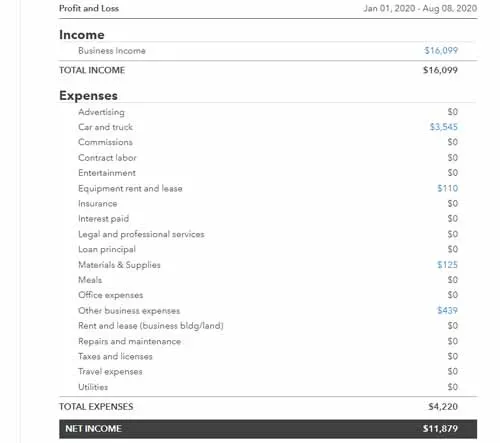

If you want a sample, here’s a couple of Profit and Loss statements from my playing around with a couple of different programs. The first one is from Quickbooks Self Employed. One thing about QBSE is it doesn’t have the ability to break out the income by type.

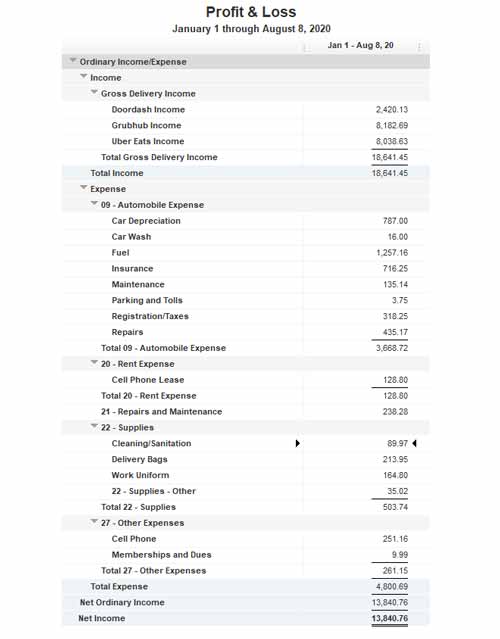

Here’s another version that I generated from Quickbooks desktop. Quickbooks online or the desktop cost a little more but they have more flexibility to show custom categories.

These can be a guide if you are creating your own Profit and Loss.

Step 3: Back it up with revenue documentation

Anyone can put together a profit and loss statement and just make things up.

Banks and management companies want more than just that. This means you want to back it up.

After all, this is about VERIFYING your income as a contractor for Grubhub or Doordash or Uber Eats, Lyft, Instacart, or any other gig company.

How can you show mortgate or auto lenders, or apartment managers/owners that the income you are presenting is legitimate? What can you provide to give them confidence that you REALLY ARE making the money that you say you are?

Here’s an example of documentation requested by Churchill Mortgage when you are applying for a mortgage. Note that they ask for your personal tax filings AND your business tax filings (for most of us the business taxes would be our Schedule C). The main thing is, you want to back up anything you claim especially when it comes to revenue.

There are a couple of things in particular you can provide.

Previous Tax Returns

This is particularly helpful if you’ve been doing gig work for a couple of years.

The following will be helpful:

- Your tax returns for any years you were self employed

- Your Schedule C for your self employment business

- Copies of your 1099-Misc or 1099-K statements

If you’ve been doing your gig work for awhile, the tax returns help you prove that you’ve been profitable consistently.

These also provide a form of backing for your profit and loss statement. If your P&L shows that you had $18,000 in revenue through 8 months, and your previous tax returns show $30,000 annually, that provides enough of a pattern to say that the money you’re claiming is not out of line.

Documentation from the gig companies.

As lenders look at your income as an independent contractor, they’re not looking at Grubhub and Doordash etc. as your employers, but more like they are your customers. These are the ones paying your business for what you do.

When I was in telecom, sometimes we needed to provide contract information or statements showing the revenue received from our main income sources. This is what you are doing here.

If you have any documentation available to show that the money you are claiming is legitimate, you want to provide that documentation. Here are a couple of samples:

For Uber, you can log in at Uber.com, click on Tax Information, and then go to Monthly Summaries and then you can download each of the monthly summaries for the year.

With Grubhub, they email a weekly pay summary. Print all of those out for the year.

With Doordash, there’s…, um, well…. Okay, Doordash is not much help. While you can pull up the earnings summaries on the app, Doordash doesn’t provide much beyond that. That’s where you’ll have to rely on the third form of documentation. I’ll say more about Doordash in a bit.

Bank Statements

Any bank statements you have showing the deposits from the gig companies will help you show you actually received that money.

If you use a debit card for quick pay, make sure you pull up statements for those.

The main thing is, you want proof that the money you said has been coming in HAS actually been coming in. Your bank statements are the best way to provide that proof.

Why you want to strongly consider keeping a separate bank account for your business.

With gig work, it’s real easy to mingle business and personal income. We’re used to getting a paycheck into our bank account, so the payments from gig companies feel a lot like that paycheck.

I know one reason a lot of people aren’t comfortable with providing bank returns: bank returns reveal your personal spending. You might be okay with letting an impersonal mortgage company see that, but your apartment manager?

The very best practice when running a business (and do I need to remind you? You ARE running a business!!!!) is to keep your business and personal accounts separate.

This is especially true when it comes to documenting your income. What I really recommend is, have all your gig earnings come into a separate account for your business. Take money out to save for taxes and operating expenses. Then pay yourself whatever is left as a form of paycheck and THAT payment is what goes into your personal checking account.

Some tips to consider when verifying income for your Grubhub, Doordash, Uber Eats, Lyft, Instacart, and other gig economy contracting.

I mentioned the three steps:

- Understand what your business income is – which is your profit.

- Put together a profit and loss statement.

- Provide documentation of the revenue for your business.

Those things will help you go a long way towards getting approval if you are applying for a loan, mortgage, or simply to rent an apartment or house. But here are a few other thoughts.

Some places won’t accept anything less than an actual pay stub.

Some lenders and some apartment managers and owners operate with a very narrow and limited set of requirements. Many of them won’t look at all beyond whether you can show them a paystub for a job.

If you run into one of those places, think of it this way. You dodged a bullet.

That sounds like sour grapes, I know.

The thing is, when anyone you are dealing with, in any kind of contract, is that narrow when it comes to what they require, there’s a good chance they’re going to be difficult to work with in other areas.

Times have changed. Self employment income is far more common. If they aren’t keeping up with the times, you may not want to get into a long term arrangement with them.

You want to make sure that your income you are reporting lines up with your taxable income.

It’s tempting to only report the income, and say you don’t have much for expenses.

But these folks you are working with know that’s not realistic. If you appear to be leaving information out, that’s going to work against you.

The other side is, if you are saying that your profits right now are on line for $50,000 a year, but your Schedule C for last year says you had no profit, you’ll have some explaining to do.

Chances are you won’t be able to explain.

Unfortunately, you can’t have it both ways here. You can’t tell the government you made no money and avoid taxes and then get a lender to believe you’re making a ton.

You should be tracking your ACTUAL car expenses as well as your miles.

I know that seems off topic.

This kind of balances some of what I said in that last section. The reality is, when we use our cars as much as most of us do, our real profits are often a fair bit higher than our taxable profits.

Look at the second P&L that I showed above (the more detailed one).

Notice the detail on the car expenses? All of my fuel, registration, insurance and other costs are listed and broken down. I even have depreciation figured in.

The actual expense comes out to 33¢ per mile.

If I were to only list the 57.5 cents per mile that the IRS allows in 2020, my profits would be $2500 less. In other words, my actual income would look like it’s $2500 less than what it is.

You want to track both. You want to document both – mileage amount AND actual costs.

I know I just said above that you want to line up with your taxable income. But if you have good records and good documentation of what your ACTUAL costs are (and you’re taking everything into account like depreciation) you can demonstrate that you’re actually earning more.

Remember you may not qualify.

The sad reality for a lot of gig workers is, they’re not really making as much money as they think. All they see is the money coming in. They don’t realize how much it’s really costing them to do this.

Unfortunately, if that is you, that could mean you don’t qualify for whatever you are applying for.

Banks are picky that way. They’ve seen too many people unable to keep up with payments because they weren’t making as much as they thought they were. That’s why they want to verify income.

While it would suck to be denied, it could be the best thing that happens to you. That’s because it can be a wakeup call.

It can help you realize that you’re not making what you thought. That can either wake you up to where you start thinking about how to actually BE profitable, or maybe it just makes you understand that other sources of income actually are better.

Being on multiple platforms is really in your best interest here.

Remember, you’re applying based on business income.

If you have multiple sources of income, that’s going to look better on your application.

If all you do is Doordash, and then something happens to your ability to deliver for them, you’re screwed. However, if the bank or management company sees that you also have significant income from Uber Eats (referral link) or Grubhub, they’re more comfortable that you’ll continue to be able to make the payments.

Oh yeah… that bit about verifying your income with Doordash.

Doordash has a spot where you can supposedly request documentation of your income.

It’s a croc.

Maybe people get a legitimate response. I’ll tell you about my experience.

On that link I shared above, it gives you a place you can click to file a case asking for documentation. I clicked it. I filed the case.

The response?

Thank you for bringing this issue to our attention. I’m sorry to hear you’ve run into some issues while using the Dasher App, but I’ll be happy to help get things working smoothly! We include a list of our recommended troubleshooting steps on the Dasher Help Center. Please review the Dasher Help Center App Troubleshooting page and follow the instructions to resolve this issue.

Doordash response to my request for income documentation.

I responded back that it’s not about the app. They replied asking me to verify my date of birth. Then they contacted me and told me I could get the information in the app by clicking on earnings.

In other words, all I can do is get screenshots off the app.

And oh, by the way… I can only go back a few months. I can’t even get a full year’s worth of data off the app.

Final thoughts on verifying your income for a car or mortgage loan or apartment lease application when you contract with gig companies like Doordash, Uber Eats, Grubhub, Lyft and others…

I’ve heard from others who had a similar experience to mine when requesting info from Doordash.

Maybe some people get what they’re looking for. Maybe I should try it again now to see.

But there’s a lesson in that:

Don’t rely on Doordash. Or Grubhub. Or any gig company.

Remember you’re not an employee. Think of it this way: Do you ever get any request from Walmart asking you to document the money you spend with them so that they can verify their income?

That’s an extreme example but it makes the point. The thing is, under this structure and in this environment, Grubhub, Doordash, Uber Eats etc. are your customers.

If you as a business owner are doing what you should be doing, and keeping good records OF your business, you’ll have all the documentation you need. Even when your customer is a turd like… well, you can guess who.

How to Verify Your Income as an Independent Contractor with Doordash, Grubhub, Uber Eats, Postmaes, Lyft, Instacart

You're applying for a loan, or you need to verify your income for an apartment, but the bank or property management won't accept your income as an independent contractor with Doordash, Uber Eats, Lyft, Grubhub or others. What do you do?

These three steps will help you understand how to verify your income as a self employed individual.

Materials

Instructions

- Explain right away that you're self employed. Do NOT go in saying you're employed by Grubhub or Doordash or any of these gig companies. Present your income as business profits, not wages.

- Provide business records. Put together a profit and loss statement for your business. Use an accounting program like Hurdlr or Quickbooks Self Employed if you don't know how to make your own.

- Document your earnings. Your Schedule C for previous tax years and bank statements will show that there really is money coming in for your business.

Notes

Some lenders are not flexible when it comes to using self employed income. If you run into someone like that, move on. Find someone who will. You're probably dodging a bullet if they're that inflexible. Often it's a misunderstanding more than their inflexibility. If you state that you're employed, they want employment documentation. If you present things properly and accurately to begin with you avoid confusion.

Recommended Products

As an Amazon Associate and member of other affiliate programs, I earn from qualifying purchases.